【CS2】Ch06 Survival models 生存模型

本文介绍生存模型,属于CS2第六章的内容,也是学习CM1的寿险精算部分的先修内容。

本文不仅适用于英国精算师的考试,Jackie 在写这篇推文时也参考了北美体系的内容,所以考SOA的同学也不妨看一下。

Notation

cdf of

sf of

pdf of

Relationship between

Events that are equivalent (important relationship between

cdf of

sf of

pdf of

Chaining Survival

Conditions on

Assumptions on

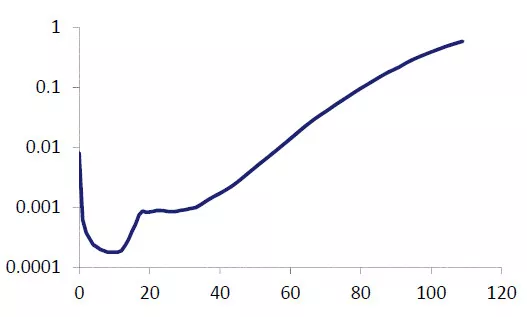

The force of mortality

Typical

- High infant mortality

- An ‘accident hump’ at ages around 20

- The nearly exponential increase at older ages

Some Common Mortality Models

- Exponential Model: Constant force of mortality

- De Moivre Model:

- Compertz Model

- Generalized (or Modified) De Moivre Model

Actuarial Notation

Survival:

Mortality:

Deferred Mortality:

It's convention that

3 ways to calculate

Relationship between F and f

Approximate

For small

Distributional Quantities of

Mean of

Complete expectation of life:

Median of

This is the value

正在检查 Disqus 能否访问...